| | | | Information and Resources for Your Business and Life | | | | Inspiration, Tools & Tips! NOVEMBER 2021 | | | | Financial Planning and Management is NecessaryFour your business, your church and for you.

Believe it or not, a financial plan is necessary to meet any goal. Whether it is in your business, in your church, or just personally. A financial plan provides a step-by-step approach to manage the finances needed to reach any destination in life. It acts as a guide as you go travel along your journey. Essentially, it helps you be in control of your income, expenses and investments such that you can manage your money and to achieve your dreams and objectives. | | | |  December December

| | | | | | | | | | Welcome back. Did you change the way you handle the mistakes that were made by others? Are you extending the same courtesy to others that you want extended to you? Always remember if you are willing to acknowledge, correct and learn from mistakes, you can actually help others in your business, your church and just in your life, do the same. This month, we will talk about the need for financial planning. As you close out the year, taking a look at how you manage your finances is a great thing to do.

| | | |

As I do every month, thanks to everyone who reached out. I get more and more excited as I see what God is doing with and in my business. It is an honor and a pleasure to give you tips and help you learn from my successes and failures. Please stay subscribed to receive more information, success stories, tips, freebies and much more.

| | | | | | | |

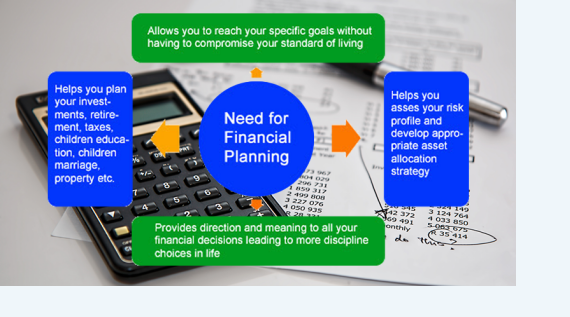

Financial planning can help you reach your goals throughout your life. Whether you want to buy a house, save for college or advanced education, live a fulfilling retirement, leave a legacy for your children or make a difference for a charity. Financial planning can help you set your goals, provide a roadmap to reach them, and identify any strategies you need that can help you get there. When thinking about financial planning there are some questions you should ask yourself about money. Some of those finance questions are in the freebie section.

There are many practical benefits to financial planning. Here are just a few. 1. Financial Planning manages how you spend and save. No matter what you are trying to accomplish, you cannot do it without money. The Bible says money answers all things. Whether or not you believe it, it is true, and it is wise to take the necessary steps to plan for success. Planning helps you to: - Increase your savings

When you create a financial plan, you get a good deal of insight into your income and expenses. You can track and cut down your costs consciously, which increases your savings in the long run.

- Enjoy a better standard of living

Most people assume that they would have to sacrifice their standard of living if their monthly bills and the monthly loan repayments are to be addressed. With a good financial plan, you would not need to compromise your lifestyle. You could achieve your goals while living in relative comfort.

- Be prepared for emergencies

Creating an emergency fund is a critical aspect of financial planning. Here, you need to ensure that you have a fund that is equal to at least 6 months of your monthly salary. This way, you don’t have to worry about procuring funds in case of an emergency or a job loss.

- Attain peace of mind

Financial planning helps you manage your money efficiently and enjoy peace of mind. Don’t worry if you have not yet reached this stage. If you are on the path of financial planning, the destination of financial peace is not very far away.

2. Financial Planning set you up to accomplish your life goals. You cannot ignore the importance of personal financial planning. It is not just about increasing savings and reducing expenses. Financial planning is a lot more than that. This includes achieving your future goals, such as: - Wealth creation

The rise in the price of everyday items means that if you want to maintain or increase your current standard of living in the future, you need to create a sufficient amount of wealth. You may also want to purchase a better car or a new house in the future; all this requires money. It is possible to achieve these goals by carefully planning.

- Retirement planning

For some of us, retirement is close, for others it is far away. However you don’t wait until it is time to retire to plan for it. If you want to enjoy a happy and comfortable retired life, you need to start building your safety net right now. For those whose retirement is far a way, planning at an early stage in life can help secure your future against financial uncertainties.

- Education Expenses

Education has become very expensive. In the future, this cost is only going to rise. This is why it is necessary to plan. If it is for your child, start the moment your child is born. If it is for you because you did not go to school after graduation or you want to go back, you have to plan.

You can make the first step to create a successful financial plan yourself.

1. Understand your current financial situation Determine the status of your current finances, your income, expenses, debt, savings and investments. This is the first step in financial planning, as it gives you a good sense on the state of your finances and ways to improve.

2. Write down your financial goals Ask yourself: ‘what are the different financial goals I wish to achieve in life?’ Write them on a piece of paper. Don’t hesitate to put down any goal because no goal is too small or too big. However, make sure that your goals are smart. (There is a smart goal sheet in the freebie section).

3. Look at the different investment options There are numerous investment options available to investors. To name a few, stocks, bonds, mutual funds and exchange-traded funds (ETFs), bank products, options, and annuities. Different investment avenues help investors to achieve different goals. When it comes to investing, I do not recommend you tackle this alone unless this is your field. This months featured company provides investment advice.

Benjamin Franklin has rightly said, “If you fail to plan, you are planning to fail.” You may have several financial goals you wish to achieve but to reach them at the right point in life; you need to have a financial plan in place.

There are resources in the freebies this month you can use to help you on your path to developing a financial plan. | | | |

Business Application Building a business financial plan is not as hard as you would think. However, it requires effort, good data, and a fair amount of imagination. And if you’ve never done this before, you’ll likely hit a few roadblocks along the way.

What is business financial planning?

Your company’s financial

| |

Ministry Application

Do you have a financial plan for your church/ministry? You should; read the parable of the talents in Matthew 25:14-30. If not, managing the finances may make you feel overwhelmed. Love it or hate it, your church must manage money. If your church is larger, you may have the resources to delegate this work to a trained staff member or outsource your needs to READ MORE ... | |

Personal Application

From your personal perspective, take a minute to read the business information. When you do, you will probably understand your need for financial planning. The question you most probably will ask yourself is, “Do I Need A Financial Advisor Or Should I Do It Myself?” Deciding whether to get a financial advisor or manage your own money is a big

| | | | | | | | Pamela Russell Ministry Information Prayer Line Name: “At God’s Door” Number: 951-981-7721, no passcode is needed. Time: 5:30- 6:00 a.m. EST, but you can log on earlier. Days: Sun-Sat, including holidays

If you want to be a part of prayer, but its a bit too early for you. Please listen and be blessed. The recordings can be found here.

Additional Information: Online information about the prayer line Prayer Requests: Submit them here. Current Devotional we are using: “Teach My Hands to War”. Access the entire year. Please come and share with us.

We have put together a wonderful project to bring healing.

You can listen to it here.

Recently we were approved so you can now also listen to it or download it from You Tube.

| | | |

FREEBIES

Here are this month’s free business and ministry tools:

- Financial Questions

Here are the questions that you should ask yourself about your financial status. Answering them will help you understand the need for a financial plan.

- Business Marketing Budget

This sample budget is an excel spreadsheet. You are provided a pdf of the sheet. If you want the actual sheet for you to work in, you can email me.

- Church Budget

This sheet is for you to use to plan your church budget. It has parameters in it that the standard business budget does not have.

How do you know if you are handling someone else's mistake in a healthy manner. Ask your self these questions.

| | | | FEATURED COMPANY/CLIENT REVIEW | | Nicholas T. Simonic is the President and C.E.O of Simonic, Simonic, Ratnecht & Associates, Inc. His experience spans all phases of corporate, estate, personal, and other tax matters. Nick's expertise in auditing has taken him into working with a wide range of entities, including schools, not-for-profit organizations, construction companies and churches.

8750 Perimeter Park Boulevard

Jacksonville, FL 32216-6347 Phone: 904-928-1040 Fax: 904-928-0909

| | | | | | If you have done work with me, please submit a review, it would help me greatly.

Please click here. You will find a list of business review sites. Click the name of the site where you want to leave a review. You can place your review on one or as many as you like. Each review will help me so much, so I am thanking you in advance. If you want to leave a review for a site that is not listed, please contact me and let me know which site. | | | | The financial planning process is necessary, and the plan is a live document. You need to monitor if and how your plan is working and do it regularly. If your plan is not working the way you envisioned it, you may need to rework some items on it and replace them with something you and/or your advisor thinks will work better. You also need to follow your plan because, as you grow older, your goals and dreams grow. It is never too late to start. Why not create your plan today. If you have questions or need any assistance, email us. You can also call us @ 904-830-0737. You can also set up a free consultation. | | | | | | "It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.” - Robert Kiyosaki | | | | MORE From Business Development

and experience to create your plan, it’s not simply a copy/paste of your accounting data. Instead, you look at your business goals and define the level of investment you’re willing to make to achieve each of these.

Business financial planning is essential to building a successful business. Your business plan dictates how you plan to do business over the next month, quarter, year, or longer - depending on how far out you plan. It includes an assessment of the business environment, your goals, resources needed to reach these goals, team and resource budgets, and highlights any risks you might face. While you can’t guarantee that everything will play out exactly as planned, this exercise prepares you for what’s coming. Here are some benefits of financial planning for business: 1. Clear company goals

This is really the starting point for your whole financial plan. What is the company supposed to achieve in the next quarter, year, three years, and so on?

2. Sensible cash flow management

Your financial plan should also set clear expectations for cash flow - the amount coming in and out of the company. In the beginning, you’ll of course spend more than you make. But what is an acceptable level of expense, and how will you stay on track?

3. Smart budget allocation

This is obviously closely related to cash flow management (above) and cost reductions (below). Once you clearly understand the amount of funding, you have to spend - whether through sales income or investments - you need to figure out how you’ll actually spend it. Get a marketing budget template in the freebie section.

4. Necessary cost reductions

Aside from setting out how much you can afford to spend (and on what), a financial plan also lets you spot savings ahead of time. If you’ve already been in business for some time, building your financial plan involves first looking back at what you’ve already spent and how fast you’re currently growing.

5. Risk mitigation A crucial aspect of the finance team’s role is to help companies avoid and navigate risk. While plenty of risks are hard to predict or even avoid, there are plenty that you can see coming. Your financial plan should make room for certain business insurance expenses, losses through risky inefficiencies, and perhaps set aside resources for unexpected expenses.

6. Crisis management

The first thing that happens in any company crisis is you review and re-build your plans. Which, of course, means that you must have a clear business plan in the first place. Otherwise, your crisis response is simply to improvise. What you probably learned through this pandemic is nobody truly knows when the crisis will end, or how it will have affected their business. Stay ahead by creating new financial plans on a monthly or quarterly basis, at least. Once you have a plan, you will find reviewing and changing it will make this process easier because you are not starting from scratch over and over, and you’ve already identified obvious risks and what to do in the event of one.

7. Smooth fundraising

Whether you’re a brand new startup, a sustainable company that needs a small cash injection, or looking for a significant series-level investment, at some point you’ll likely need funds. And the first thing any prospective investor or bank will ask you for is your business plan. They want to see how you intend to grow the business, what risks and uncertainties are involved, and how you’ll put their money to good use. A financial plan is critical, and the better your history of planning is, the more likely they’ll trust your projections.

8. A growth roadmap

Your financial plan helps you analyze your current situation and project where you want the business to be in the future. Again, your wider business plan will do this on a broad level. The financial section adds data to these goals, and plugs in your level of investment along the way. | | | | MORE From Ministry Development

an accountant. For many smaller ministries, financial planning and managing the money may take a little more finesse. You might not know a lot about church finances’ best practices. You may have a volunteer, a reluctant member of your staff who does this part time, or even the pastor or the pastor’s wife overseeing your church’s finances. Keeping track of donations and expenses, following church financial management best practices, and even knowing where to start or where you’re going as a church is challenging if you don’t have adequate time or the right training.

Please read the information for the business financial planning. In addition, here are some tips for financial planning for your church/ministry’s finances.

#1. Learn the basics of budgeting

The best way you can steward your church’s financial resources is to create and follow a budget. (There is a church planning budget in freebie section) Unless you were trained as an accountant or have experience with managing budgets, as a pastor or volunteer, you don’t need to worry about becoming a certified public accountant (CPA). Your goal is to know the basics of budgeting, which are reasonably simple and never changing. To help you think through your church’s budget, assess the current state of your finances by reviewing the last 1-3 years of your financial statements. During your review, you also want to look at the trends in your church’s attendance and giving. Monitor whether your church is experiencing a gradual or sharp increase or decline in giving. It’s a good idea to know where you’re at before you move ahead with significant financial decisions.

#2. Keep track of your donations and expenses

Do you clearly understand your church’s finances? Church finances best practices require that you, your staff, or a volunteer will need to keep track of how many donations your church receives (revenue) and how much money your church spends (expenses). Another significant trend to track in your church is how much the average member donates.

#3. Set up recurring giving

What if you could know how much someone was going to give to your church every month? This would make your budgeting process and church financial planning significantly easier. Leading your church to automate their giving will help your church budget—and it will help you build a more generous church culture. This also makes church financial planning easier because you can plan with greater certainty and set your budget for the year. - “How does automated giving improve our church’s finances?”

- In general, people who sign up for recurring giving donate more frequently and donate more per year.

- For your church, automated giving creates a steady and predictable source of donations.

- Also, data from Network for Good shows that donors who set up recurring contributions give 42% more annually versus those who make onetime donations.

#4. Protect your church’s integrity

It’s essential for your church to have a variety of safeguards in place to protect the integrity of your church and those who handle the finances. Here are a few things for you to consider: - Require dual signatures

- Limit access to bank information

- Reconcile your ledger

- Encourage volunteer rotation

- Coordinate an external audit

- For additional financial security, Aubrey Malphurs and Steve Stroope recommend removing your church’s senior leadership from being directly involved with the church’s finances. This idea may not be possible for your church. But if you can make this move, it will provide you with an added level of financial integrity. This arrangement can give the members peace of mind, knowing that the leadership does not use their donations to determine how involved they will be in a donor’s life.

#5. Save for a rainy day

It’s a good idea for your church to have a financial cushion. As you know, your church will have unexpected expenses or your church may experience an extended decrease in giving. Even though there are arguments for and against a church having financial reserves, it’s a good idea for your church to build a reserve of cash for emergencies. Based on a survey conducted by Christianity Today’s Church Law & Tax Group, the average church set aside 2% of their annual toward building their cash reserves, which is another good benchmark for you to keep in mind. As you build your cash reserves, aim to save enough for your church to cover 3-6 months of expenses.

#6. Talk about giving with your church

As a church leader, you have to walk a fine line when it comes to talking about money—you can talk too much or too little about your church’s finances. In your church, there are two groups of people you need to keep in mind when sharing financial information: your congregation and your leadership. Regarding to your congregation, it’s hard to say how much is too much or too little to share. Some churches share weekly updates, whereas other churches may share a financial update once per month, quarter, or year. However often you choose to update your church is up to you. Just aim to be consistent with your frequency. Updates are also helpful if your church has a financial emergency. Talking with your leadership will give them the information they need and ensure that everyone is on the same page. You can regularly share financial information with your leadership by including a financial update in your regular business meetings. You don’t need to go through every line item in your budget necessarily. But you should consider discussing these three items along with an estimate of the percentage of your budget used for each category. (The percentages listed are the general average):

* Personnel: 33-45%

* Building/Facilities: 25-30% * Office Expenses: <10% | | | | MORE From Personal Development

decision. Not everyone needs an ongoing relationship with a financial planner or investment advisor. Here are a few signs you may need a financial advisor.

• If you are not sure, you will really do your financial planning yourself.

Properly planning and managing your finances, making the right financial decisions takes time, skill, and effort. It’s not a onetime thing, either. Time is our most precious commodity. There are plenty of things in life you could do, but it doesn’t mean you’re going to do it. You have a lot on your plate. Finding time to research financial questions, evaluate your options, and execute a decision takes time.

Even if you could make the time, personal finance isn’t interesting to everyone. However, if you’re neglecting your finances, it’s likely worth it to hire a financial advisor. Time is money, and there’s a cost to delaying good financial decisions or prolonging poor ones.

• If your strategy a blend of winging it and Google

You don’t know what you don’t know. If you’re just Googling for answers to specific questions, how will you know you didn’t miss anything? You can find the greatest risks facing you financially aren’t even on your radar. Your financial life is complex and inter-related. Pulling one lever can have unintended consequences in another aspect of your life. How can you be sure you’re going to get the best outcome if you haven’t done it before?

• If your finances are disorganized, you don’t know where you stand, and you don’t have goals.

If your accounts are scattered across multiple institutions, it’s hard to know where you stand financially. Particularly if you don’t have a saving or investment strategy. This is another situation where you might need to get a financial advisor instead of doing it yourself. Getting organized and building a strategy going forward is a critical step. But it doesn’t just end there. You must implement it, stay on track with savings goals, and/or revise plans when things change. Without ongoing support, recommendations likely sit idly in a desk drawer.

• If you are about to make a life-changing decision. We have a lot of flexibility to unwind many of the decisions we make. But you can’t always rely on a take-back, especially for major financial decisions. You may need the tools, experience, and objectivity a financial advisor can bring to help you make the best decision the first time.

Please keep in mind, a comprehensive financial plan can help you make big financial decisions A financial plan helps accomplish four major objectives: 1. Answer the big questions. If you’re contemplating a big decision like can I retire at the end of the year, should I use a windfall to pay off my mortgage early, or how much do I need to save to retire and maintain my lifestyle, a financial model is the best way to evaluate the goal and compare alternatives.

2. Incorporate the various ‘side effects’ of deciding about your money or investments, like tax implications or funding one goal at the expense of another. Looking at it in a vacuum won’t give you the entire picture. The only way to pull it all together is through a financial plan.

3. Considering and quantifying alternate paths using what-if analysis. Who doesn’t like options? Maybe you have your heart set on retiring at 55. Wouldn’t you want to know what your retirement budget could be if you worked another two years?

4. Stress-test your plan with a risk simulation to help ensure you don’t run out of money. By accounting for the variation in investment returns, a risk simulation can help investors feel confident knowing the probability that their plan will succeed.

If getting a financial advisor would give you peace of mind or reduce money stress, it could be worth it.

If you decide you want to use the services of a financial advisor, where do you begin? Unfortunately, sometimes figuring out you need a financial planner is the easy part. Navigating the sea of financial advisory firms, services, and fee models can feel overwhelming. Here are some questions you need answered before you chose someone.

What’s the difference between a financial advisor, wealth manager, financial planner, investment advisor, etc?

There are many synonyms for financial advisors. While there are some restrictions on who can call themselves an advisor (or adviser), it’s usually easiest to set the individual’s chosen title aside. Instead, focus on the other aspects, like services, firm structure, credentials, personality fit, fees, and so on.

How will I know my advisor is acting in my best interest? Not all advisors are held to the same standards. A fiduciary duty is the highest standard of care under the law. Only registered investment advisors always have a fiduciary duty to act in your best interest. Other types of advisors may not be held to a fiduciary standard at all or only at certain points in the relationship, but they’re not a full-time fiduciary.

How are financial advisors paid? Compensation methods vary between advisors. There three main types of fee structures: - Fee-only: A fee-only advisor is only paid by their clients; they do not sell products. Fees are most often based on a percentage of investment assets the advisor manages. So as your accounts grow, the advisor does better too. The fee-only financial advisor model is typically considered the most transparent and least likely to create conflicts of interest between the client and the advisor, as sales-based incentives are removed. While many fee-only financial advisors are registered investment advisors (and fiduciaries), it is possible for a firm to be one and not the other.

- Fee-based: Fee-based advisors are typically paid in two ways: a percentage of the investor’s assets under management and by commissions from selling products, such as life insurance, annuities, mutual funds, or other investments. In a fee-based relationship, the client isn’t the only one paying the advisor. They also receive commissions and referral fees by third parties.

- Commission only: Some insurance agents, banks, stockbrokers, or large companies may not charge the end client at all and rely on commissions from selling products instead. The relationship here will be the most transactional in nature and heavily focused on advice with a product-based solution.

How much will it cost me?

How much it costs to work with an advisor depends on the advisory firm, your situation, and services. While cost is an important component, the cheapest option today might be the most expensive in the long run. Consider how advisory fees can be offset by the financial benefits an advisor can provide and your alternatives.

What are the certifications and advisor should have? There are no specific educational requirements for individuals offering financial advice and financial planning. So additional credentials and designations can be helpful. Of course, there are no shortage of acronyms here either. The CERTIFIED FINANCIAL PLANNER™ professional designation is typically considered the ‘gold standard’ for financial advisors as the Chartered Financial Analyst® designation is to asset management. | | CALL (OR) EMAIL 904.830.0737 | help@drpamrussell.com

| | | | | | | |